Invest regularly into Stock ETF, then add Bond ETF to your portfolio when you are 5-10 years away from your retirement.

Thank you for your continued reading, hope you enjoyed the previous post about “How to save money and for how long?“. I am very happy that you are interested to learn more about our portfolio, and how you could structure yours. Our portfolio evolved over time with changes in our knowledge of financial products, tax implications due to domicile country, perception of the world’s economy, and understanding that some old adages do not apply blindly anymore. Thus, we will share with you what we had, and what I would suggest so that you can avoid making similar mistakes as we did. Fingers crossed.

Stocks and Bonds, what are they?

Stocks, or equities (‘Actions’ in French) represent a share of a business. Usually, its objective is to make profit, alongside other objectives it may have. These profits are shared among employees (through wages and bonuses), governments (through taxes) and shareholders (through price appreciation and dividends). What you can get as shareholders is very dependent on the performance of the company. As stock investment involves risks, a positive return on your investment is not guaranteed.

Bonds (‘Obligations” in French) generally represent a portion of the debt of a company or a government. It is an agreement between the bond-issuing entity and the bondholder that the entity will honor the bond par value (principal amount) repayment with coupons (interest payment) at rates specified. The riskier the bond, the higher the coupon rate. Usually, when investment advisors mention bonds in a portfolio, it refers to government bonds, not corporate bonds. Mama FC and I used to prefer corporate bonds because of higher yields. However, we realized that corporate bonds are too correlated to equities. Additionally, and they do not offer the expected protection against a stock market downturn. The objective of having a balanced portfolio is to minimize correlations among asset classes. Consequently, corporate bonds, especially the high risk ones, may not always be suitable.

What is a portfolio?

A portfolio is a mix of assets with objectives to either have value appreciation over time, or provide a stream of income during the life of the assets. There are many variables to consider when you build your portfolio:

- Asset class: stock, bonds, exchange-traded funds (ETF), commodities, real estate investment trust (REIT), trust, real estate, cryptocurrencies, collectibles…

- Asset type: spot, option, future, perpetual

- Asset location: world, developed economies, emerging markets, eurozone, or a specific country

- Industry: diversified, or concentrated such as retail, energy or technology

- Theme: ESG, sustainability-linked have been attracting lots of attention and money recently

- Asset currency: USD, EUR or your home currency

- Cash: with or without cash positions

Once you know what you are looking for, you can usually find a financial product which combine the variables. As an example, it could be a Global Spot ETF focused on energy, priced in USD. Then you can combine these products with a specific weight for each asset to create your own portfolio.

It looks complicated, can you do it for me?

Does it sound like a daunting task, or you do not know where to start? Let’s tackle it one step at a time.

Below I will detail more on ETF investing because it is the financial vehicle that we are more familiar with, and also what we used to reach FI (for the first time). It was also an optimal solution based on where we lived at the time of accumulation. With a different country and different market environments, some people may use real estate investments to reach FI. There are no right or wrong answer as long as you make it right? I actually flipped two apartments in Paris (bought, remodelled and sold) at the beginning of my career without knowing that it could be an alternative source of income, even a career for some.

What is an Exchange Traded Fund (ETF)? I just want to buy Tesla and Walmart stocks!

If you are fully convinced that these companies will be leading the world economy in the next 30-60 years, go for it. However, it might be risky to put all your savings in a handful of companies. Even if there are great performers now. Having gone through the phase of trying to hand-pick stocks, we are very inclined to keep investment as simple as possible, and invest only in ETFs.

Key market indexes only contain the TOP companies

Some people are also concerned about missing out on the next Amazon or Google in their portfolios. The beauty of buying a S&P500 index, lies in the fact that the index tracks the Top 500 U.S. companies. Similarly for the Nasdaq which tracks the Top U.S. Tech companies. Some companies will join the club, and some will be removed from these lists. This self-cleaning mechanism is fantastic. It automatically keeps only the prominent companies at the time. This type of instrument perfectly fits our FIRE community. Indeed, we should invest for the long term without having to worry about which companies are out- or under-performing.

In the beginning of our journey, our portfolio was composed of a mix of everything, individual stocks, corporate bonds, government bonds, stock ETFs, bond ETFs, REITs etc. All those investments were incorporated in different countries and denominated in different currencies- a real mess to track for us.

Over time, our portfolio has moved towards having fewer components as we aim for simplicity. We accepted that getting market returns was already a good achievement considering that we were just investing in ETFs. So we progressively sold our individual stocks and bonds, and reinvested the proceeds into stock and bond ETFs.

After reaching our FI number, we have trimmed our list of assets further by exiting all remaining individual assets, and replacing almost everything by ETFs. Our portfolio is now mostly structured around the following ETFs: CSPX, IUIT, CNDX, CBU7 and CBU0. We have kept some individual stocks that have large capital losses but can be useful when we sell. Indeed, in some countries, capital loss can be used to offset capital gains to lower our tax bill.

Simplicity, simplicity, simplicity

The FIRE community has agreed that a broad market index ETF with low fees should be recommended. Some people prefer:

- World market index: with forecast that the U.S. will lose their hegemony over time, and emerging markets will take a larger share of the world economy;

- U.S. market index: with belief that the U.S. will remain the leading economic powerhouse;

- One’s own market: either to support the development of their economy by investing in it, or invest in something one is familiar with.

Ultimately it is a personal choice. We believe that the U.S. has the infrastructure, the entrepreneurial mindset and the capital to remain at the forefront of technology and innovation for decades to come. As the adage goes, “When the U.S. sneezes, the world catches a cold”. If we look back at the Tech Bubble in 2001, the Global Financial Crisis in 2008 and Covid in 2020, market crashes largely started in the U.S., and rippled through the world. Once the U.S. economy got back to its feet, the rest of the world economy started to improve. Some readers may disagree, and only time will tell us who is right, or if we are all wrong most of the time. For us, we prefer investing in a broad-based index that is U.S.-driven while being global and simple, thus S&P ETFs are our top choices.

Consistency is key

Choosing between the U.S. or World market indices is sometimes less critical than being consistent in your investment. Indeed, if you pick one, or a mix of both, just stick to it. You should avoid changing your allocation whenever one outperforms the other. If you keep modifying your allocation by responding to market trends, you may find yourself doing the switch at the worst time. Markets go through cycles but no one can tell you when the next turn is. Being off-phase with the market while trying to time the next turn could cost you much.

Everyone mentions a 60/40 stock vs bond allocation, is it good?

For a long time, I tried to understand what balance between stock and bonds is the most efficient. Is it 60% stocks / 40% Bonds or 70/30, or 50/50? Naturally, it depends on your risk appetite. But it is also hugely affected by your time horizon.

In your accumulation phase, your weight of stocks should be heavy. The further you are from your retirement, the more stocks your portfolio should include. If you are starting your FIRE journey in your 20’s, I would argue you should not be afraid to go with 100% stocks. There are bound to be people who will have a different opinion because of their personal conviction or experience.

What we can do as investors should be to understand the fundamentals of our investments. Over the past decades, stocks (in real terms, e.g. adjusted for inflation) have outperformed bonds, and it will likely continue. This is the reward for investors willing to stomach the extra risk along the ride. I agree that in a shorter period, bonds may outperform stocks. But as a FIRE community member with a long time horizon, you may be better off with an all-stock portfolio during most of your accumulation phase.

Isn’t 100% stock allocation risky?

Of course, it is. Yet, as you are committed for the long term, you will benefit from the market dips or even better the bear markets. It is very difficult to know when to buy and when to sell, even for the best traders who trade for a living. To make the decision easier, you may implement a simple strategy: invest in a broad ETF with low fees with a dollar cost averaging (DCA) approach.

DCA is a fancy way to describe the impact of putting the same amount of money in the market at a regular time interval. It is usually once a month, or once a week depending on when you get your paycheck. As you invest in the same set of assets periodically, your cost is averaged across the different purchase intervals. The icing on the cake would be to automate this process with your bank or broker. So that once it is set, you will not have to manage any investment, nor be tempted to time the market. Remember that “Time in the market is more important than timing the market”.

What are the benefits of dollar cost averaging?

There are several benefits to be 100% in stocks while deploying DCA:

- You will become used to the volatility of your portfolio. As the market evolves with ups and downs, these market fluctuations will not affect you anymore. Or at least they will not worry you as much. Indeed, after a few years investing in a volatile market, you will likely remain calm, and treat volatilities as a natural behaviour of the market.

- When markets are down, you feel great instead. As you are still buying new assets all the time, you would benefit from buying stocks at a discount. If you stick to your investment strategy, you will be able to buy more units of the same assets with your cash. So don’t be surprised to find yourself feeling great when markets are down next time.

- You take away the perpetual struggle in choosing the best time and best price to place an order. No one can be 100% accurate when it comes to timing the market. Banks may issue buying or selling recommendations because they want customers to trade; this is the way that banks make their money through the fees they charge. For long-term investors not looking to flip trades, the best and simplest strategy is simply to buy and hold.

- You can start investing with whatever amount of cash you can spare. With ETFs, you do not need a large lump sum as compared to some other assets classes.

When should you add bonds?

I would say in your final decade of accumulation phase, you could start to add bonds on a DCA approach till you reach your target balance: 60/40 or 70/30 or 80/20 or whichever percentage allocation that you are comfortable with.

This number should also depend on your age when you retire, or another way to look at it, how long you plan to live on your savings. Expecting to live off your savings for 30 years is quite different from if you expect to live for another 60 years. The longer the time horizon, the more stocks you may expect to hold (70/30 or 80/20). Consequently, you can expect also to experience more volatilities in your portfolio. If you are anxious every time the market drops by a few percentage points, you should stay with the more conservative 60/40. There is always a trade-off. A higher bond proportion usually means a bigger FI number.

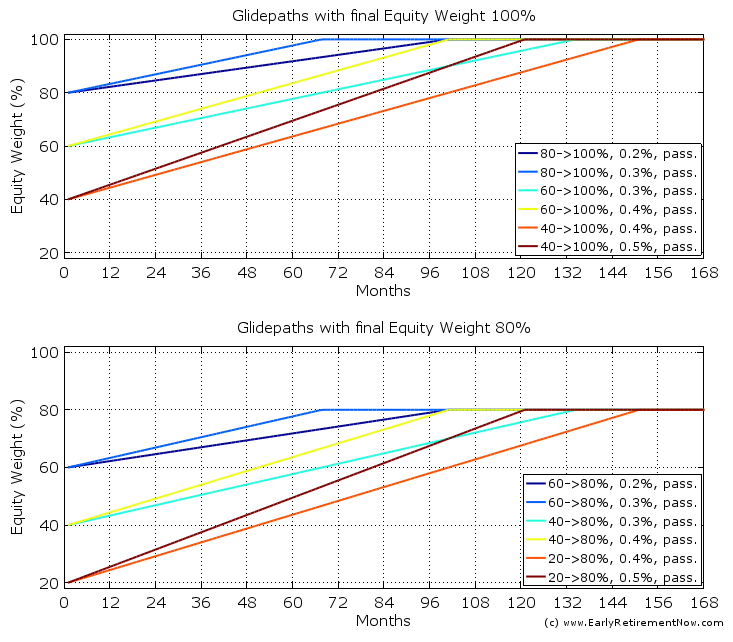

What is a glidepath or bond tent strategy?

An ultimate approach is a glidepath as described by the blogger big ERN: “The Ultimate Guide to Safe Withdrawal Rates – Part 19: Equity Glidepaths in Retirement”. If you haven’t read one of his posts, you may want to check them out. According to him, a glidepath can be described as a balanced portfolio where the stock portion increases overtime. In other words, you would start with a 60/40 at the beginning of your retirement, and progressively increase the stocks portion (either by living off your bonds, or selling them to buy more stocks) to reach almost a 100% stock allocation.

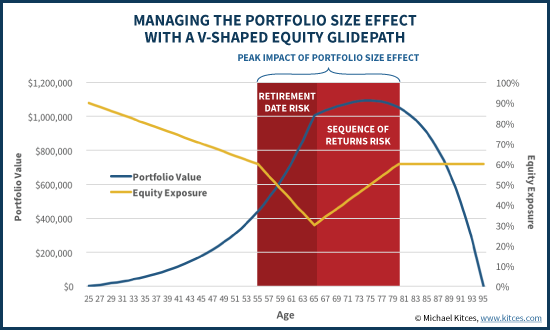

A bond tent is an allocation strategy where the bond allocation increases before retirement, and then decreases after (e.g, the stocks allocation increases). This concept was introduced by Michael Kitces in his blog post about “managing portfolio size effect with bond tent in retirement red zone”

It took me some time to understand the chart above, so take your time. It is always better to take time to understand than simply accepting someone’s recommendation. Especially when it can affect your life savings!

Although Kitces’s concept is very tempting, I would change some of his assumption to reconcile with more back-tested mechanisms developed by big ERN. First, most FIRE aspiring people (including our Firecracker’s family), aim to retire (way) before the ‘official’ retirement age. Thus I would move the 65 years old retirement age closer to 45 or even 35 for eager ones. Second, I would move the Equity exposure line up with a slightly different slope. The equity exposure before retirement would be flat at 100% until 5-10 years of retirement. In the 5-10 years time frame, I would load up with Bonds to reach your target bond allocation (60/40 or 70/30). This could be achieved by buying bond ETFs. And then after retirement, you could increase your stock exposure, by using your bonds to pay for your life expenses.

Should I be satisfied with the market average return?

When you invest in a S&P500 ETF, you can expect to earn the average return of the S&P500. Although we mention average return, this return isn’t averaging all the stocks but the companies included in the index only. I know that some people may not be satisfied with only the ‘average’ return, but it may not be that bad. Over time, these returns are often better than what you would get by stock picking. It limits our own bias in sector, weight, and all other sources of error that lead to disappointment later on. I am more than happy to get the ‘average’ of the top companies by just paying a small fee of a few basis points to trade.

When should I start investing?

Should I put money now, or wait? But wait, wait for what? It is a valid question. Of course, no one wants to put money in the market, and watch it shrink days after days in a bear market. I know people who did it, and then sold at a loss and claimed to never invest anymore. First, it is sad that they got burnt, and then second, it prevents themselves from benefiting from the rebound after.

Why “Time in the market is more important that timing the market”

The chart below aims to highlight that time in the market allows you to enjoy the ups and downs. It measures the performance of a $10,000 investment in S&P 500 stretches from 1995 to 2014. This 20-year period is long enough to be representative of market turns and cycles.

If you have invested all along, you would have a portfolio of $65,453 (or 9.85% average return per year). If you would have missed the 10 best days (which no one can predict), your portfolio would end up at $32,665 (or 6.10% average return per year). You may say that the difference between 9.85% and 6.10% is only 3.75%. You are right in the figure. However, this 3.75% compounded over 20 years accounts for $32,788! By staying in the market over 20 years, your final value is almost double compared to the same investment but missing just the 10 best performing days. The conclusion is it is best to stay fully invested especially during a storm, as six of the ten best days occurred within two weeks of the ten worst days.

Source: https://www.businessinsider.com/cost-of-missing-10-best-days-in-sp-500-2015-3?r=US&IR=T

DCA or lump sum?

Any reasonable analysis over a long period of time would demonstrate that a lump sum investment has better performance than DCA. It makes sense as in the long run, the market always goes up. By investing your money early, you end up with a bigger portfolio. I have heard of a wealth director on the radio claiming DCA as a better performer using the 2020 time frame. To me, any analysis focusing on a short period (e.g. less than 10 years) may fall prey to misrepresentation. Although DCA performance is lower than lump sum overall, I would still recommend a DCA approach especially for its strong psychological benefits mentioned earlier.

In hindsight, we might have stretched the time vs timing philosophy a bit too much, which could be irresponsible and risky, and I would thus discourage anyone to do the same. At some point, we borrowed money to invest in the market 😱😱. Any financial advisor, or simple common sense, should tell you that it is a bad idea. However, we were not investing money we did not have, we were just investing money we did not have yet. The ‘yet’ makes a tremendous difference.

Borrowing for investing? We did, but we should not have

In Hong Kong, you can borrow money to pay for your taxes. It is a gimmick as taxes are very low there (~15% on your income, and there is no tax on capital gains or dividends). Anyway, every year at the period where you are supposed to pay your taxes, banks offer “tax loans” promotions to be repaid by instalments within the coming year. Guess how much you can borrow? 20%, 50% 80% of your taxes? Ah nope. We borrowed about 5x worth of our tax bill, thus about 80% of our annual income. We took advantage of this opportunity as the borrowing rate was below 1% p.a. with some cash coupon and rebate making the loan almost free.

Both Mama FC and I had relatively good positions in large corporations with no economic challenges in sight. So we borrowed the money, paid the taxes and invested the rest as a lump sum in the market. Every month, 80% of our paycheck goes to repaying the tax loan. It was a bit risky, but it did serve us well through the 2016 to 2018 bull market.

Retrospectively, I would still recommend investing a large chunk of your salary but without the borrowing part. If you are more math-driven, I would suggest tapping Big ERN’s insight in his post, “How to invest a windfall: Lump Sum or Dollar Cost Averaging?”

In future posts, we will cover “How to invest in the long term at minimal cost?” and also “How to choose a good ETF?“

Hope you enjoyed the reading and please give us your comment below. What is the weight of assets in your portfolio and how many years are you away from FI? Are you DCA or lump sum investor? Which advice would you give to your younger self?

Tags: DCA, lump sum, ETF, Stocks, Bonds

One thought on “What is the best way to structure your portfolio?”