My humble thoughts would be to invest regularly in S&P500 index or All-World index, then add US Treasuries 10 years when you are 5-10 years away from your retirement. Accumulating ETFs are usually more tax efficient.

- S&P500 suggestions: CSPX for non-US investors, SPY for US-citizen

- All World Index suggestions: IWDA for non-US investors, VT for US-citizen

- US Treasuries 10 years suggestions: CBU0 for non-US investors, IEF for US-citizen

The previous post “How to save money and for how long?“, to “What is the best way to structure your portfolio” had many concepts to understand. We are happy that you are still motivated to the next step.

This post is focused on the details of an ETF, and how to choose the ones you want. Before diving further, let’s understand 2 key elements about ETF: Use of Profit and Fund Domicile. The Use of Profit refers to the distribution mechanism (Accumulating or Distributing) and the Fund Domicile refers to the place of incorporation (USA, Ireland, or other). They have significant impact and consequences, not only on Gain Tax, but also Wealth Tax. 😱

Accumulating or Distributing?

If you are a US-investor, you would likely not know the existence of Accumulating ETF as all ETF are Distributing. EU-investors (and all non-US investors) have the opportunity to choose among these two different strategies for the same constituents of an ETF.

Let’s take a step back and review the different ways to measure your return on investment, and which one is better. The purpose of a company is to make profit. These profits can be returned to their shareholders in several ways.

- If companies have very promising internal projects with returns higher than their cost of capital, they should invest the money internally. As the money ‘stays’ inside the company and will generate more money in the future, the value of the company increases.

- If companies don’t need all their income to invest in new internal projects, they can distribute the money back to the shareholders in the form of Dividends.

- Finally, companies can also buy their own stock (a share buy-back). This actually reduces the number of shares in the market, which consequently inflate the EPS, driving up the value of the stocks.

All these explanations are interesting, but which return is best? Price appreciation? Dividend?

It mainly depends on where you are on your FIRE journey and where you live

If you are still accumulating wealth, you don’t need the ETF to give you dividends, you want these dividends to be re-invested asap and generate more returns. In your retirement, you might prefer to use a Distributing ETF, as the dividends will be paid to you automatically and regularly.

It also depends on where you live and pay your taxes. Depending on your tax residency status, it can be an important element to take into consideration.

In Switzerland, the Tax Authority treats the accumulating and distributing ETF the same way, you are being taxed on the real dividends you received, or the ‘theoretical’ dividends that you would have received if you were holding an accumulating ETF. In that case it does not make a difference except the time it will take to fill up your taxes.

Differently, if you are living in France, you would be taxed only on the real dividends you received. So holding an Accumulating ETF has the advantage for you to choose when to cash out some money, and thus when you would pay taxes on capital gains. As you are delaying the payment of taxes, you are getting an interest free loan from the Government. Moreover, you might be able to offset some capital gains with some capital loss of another asset (something that you can not do when you receive Dividends). Thus, Accumulating ETF in France is the best option throughout the accumulating phase and also the distributing phase (eg. retirement).

Why choosing the wrong ETF can have huge Estate planning consequence?

We started our investment journey based on ETFs recommended by US bloggers. After some time spent on forums, I discovered that inheritance tax depends on the domiciliation of the asset. If you are holding US domiciled ETFs, these assets are subject to US inheritance laws. If your country has not ratified an estate tax treaty with the USA, your assets will likely take a 40% tax cut above USD$60,000!

Thus, it is very important to decide on the best domiciliation based on your personal situation. To help you in this critical task, I would recommend you to check the following page: Nonresident alien’s ETF domicile decision table from the highly valuable Bogleheads website. For most non-US countries, non-US domiciled ETFs are recommended. UCITS ETF are domiciled in Europe, likely Ireland, but sometimes France or Luxembourg and are also good alternatives. Remember to select a large fund size with the lowest fees.

How can you find an ETF?

If you want to search for ETF by yourself you can use these websites: justETF.com, Etf.com or ETFdb.com. You might find others, but these ones list most of the tradable ETF in the world. I would recommend searching for an ETF using their search function and filters. Once you have short listed a few ETF, you should also go to the official website of the ETF issuer to check the data.

But there are so many ETFs and criteria, which ones are the most important?

You should look for a market index ETF with the largest AUM (Asset Under Management ~ the size of the ETF) and the lowest fees. The larger the fund, the better the liquidity. It means that it will be easier to find a buyer or a seller to take the opposite side of your position, and also the spread (difference between the ‘Bid’ and the ‘Ask’) will be minimal. As an ETF is a commodity, there are no reasons why you should pay more for the same product. Thus, you should choose the cheapest which is available by your broker or within your retirement fund.

How to search for a specific ETF?

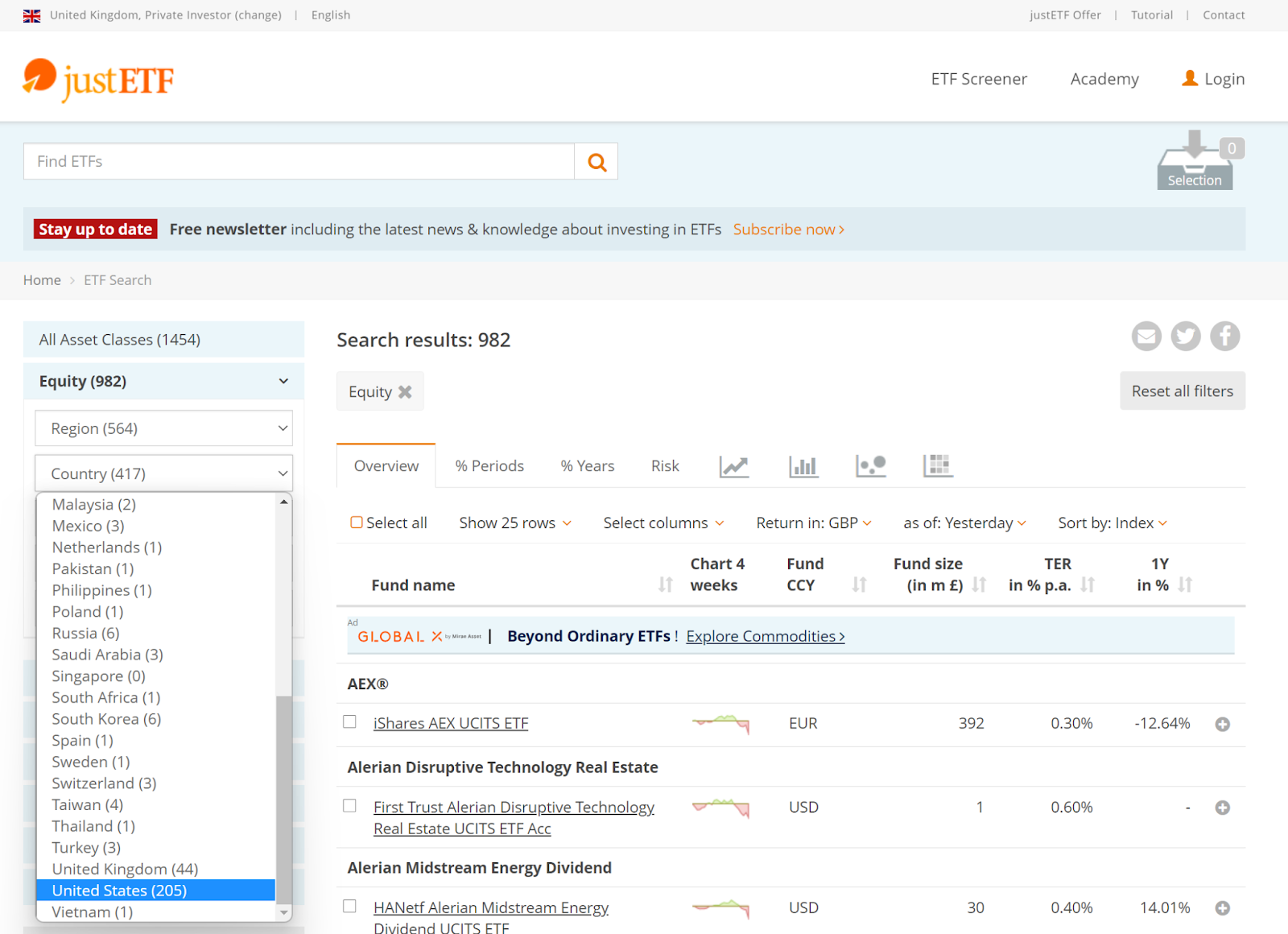

Let’s take an example. I am looking for an S&P500 ETF, Accumulating strategy in USD currency.

1. Landing page

- After clicking on “Search ETFs”, select in the list of criteria on the left side: Equity >

- Country = United States

- Matching Indices = S&P 500

- Fund domicile = Ireland

- Use of Profit = Accumulating

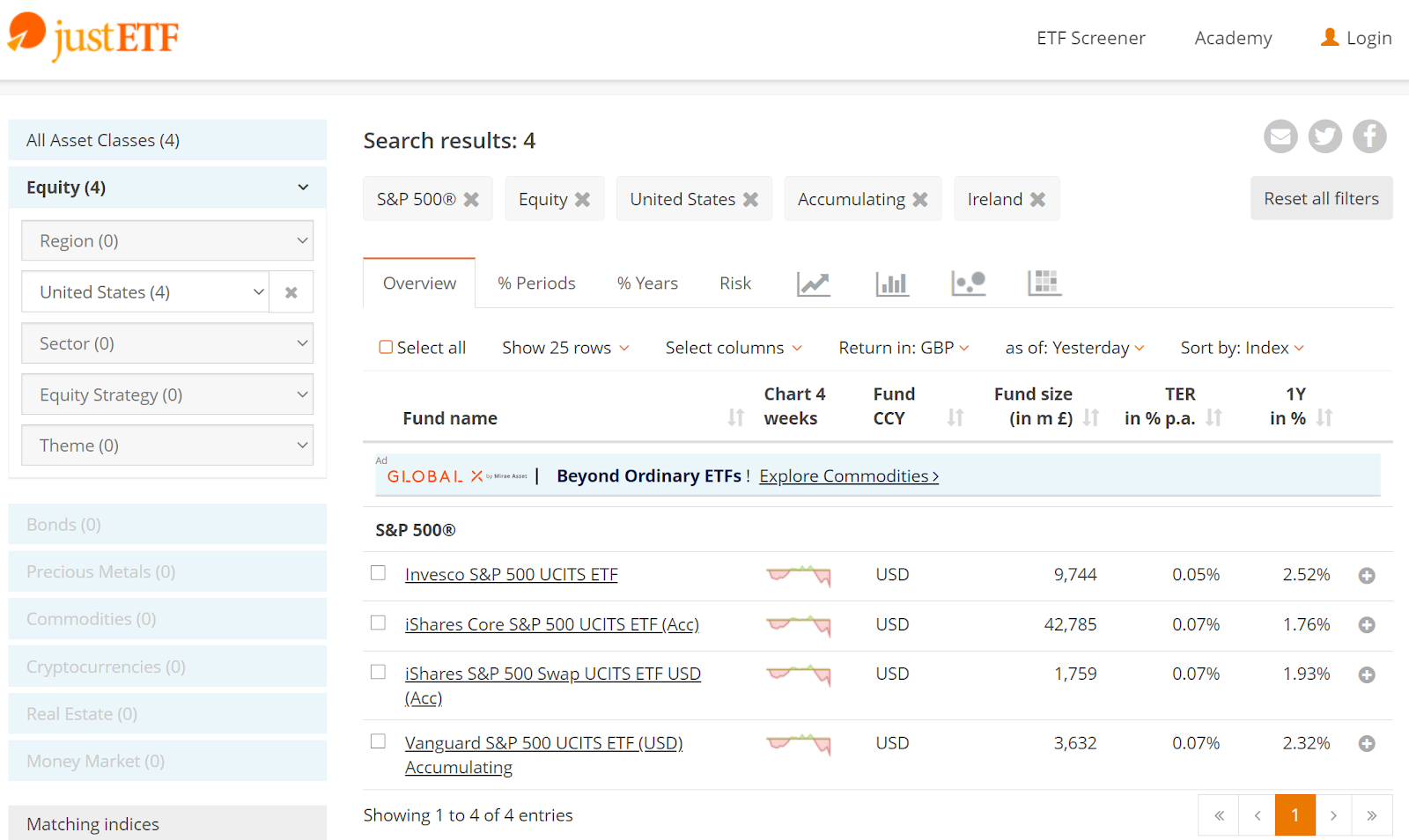

- There are 4 ETF matching the above criteria

What are the criteria that matters?

Fund size: the bigger, the better. The more assets are under management, the more investors are attracted. Consequently, the spread (between the ask and bid) will be negligible, and your trade will be almost instantly executed.

TER: It represents the fee that the ETF issuer is charging for this ETF. The lower, the better. If you invest $100 into the iShares Core S&P 500, Blackrock will charge you 7 cents annually to manage the ETF. When I recall that banks can easily charge management fees in the range of 1-2%, plus deposit fee, plus a withdrawal fee, plus plus plus…. Banks don’t want you to use these products because once you know they exist, you will never invest money into their products.

After you can click on the URL to get more details on the ETF, especially the issuer, ISIN and Ticker.

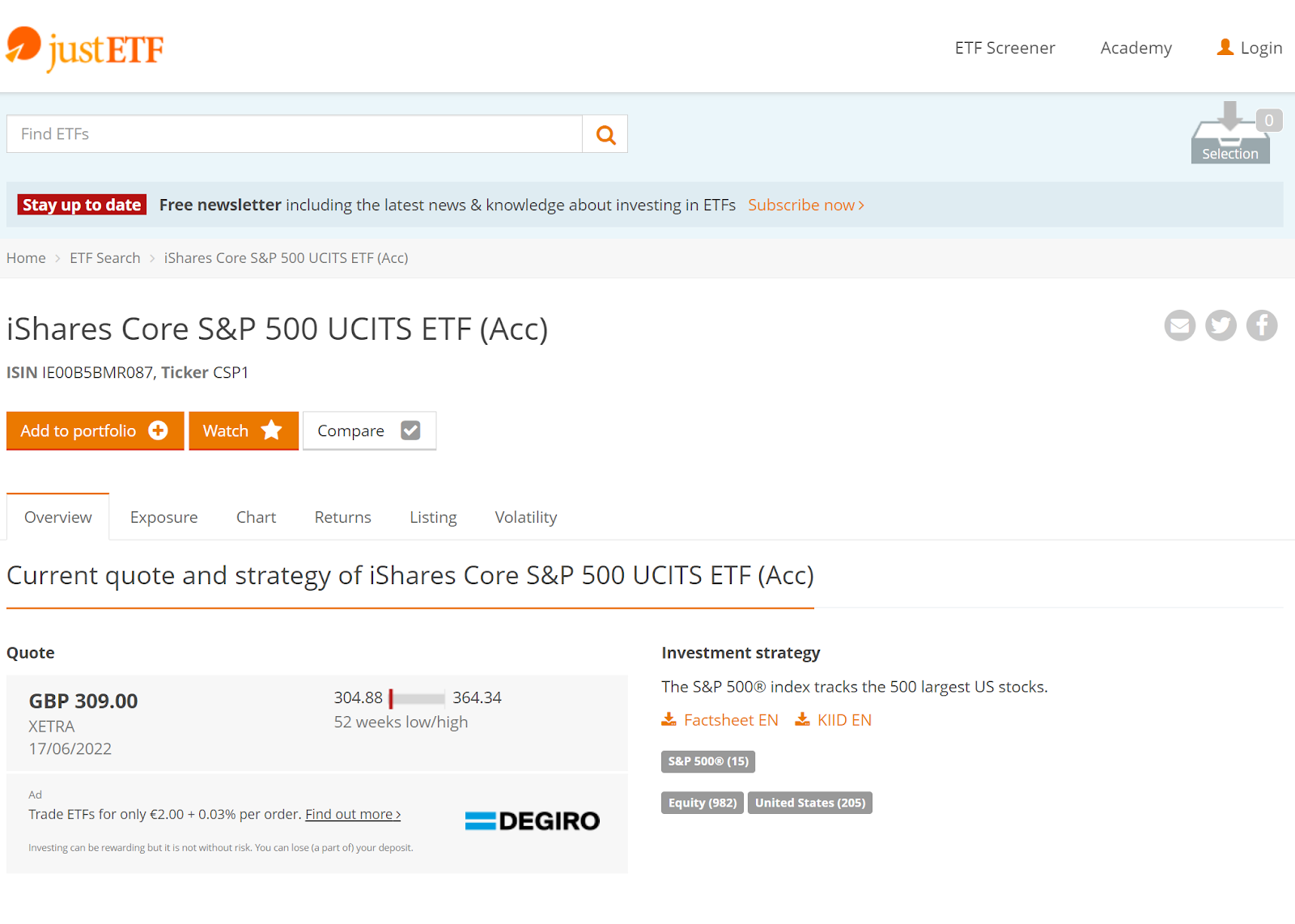

Afterwards, I will always double check the information from the official website of the ETF issuer (just copy the ISIN, and paste it in Google).

There you’ll access more detailed and updated information.

In the above example, we looked for a S&P500 ETF for non-US investors, and we found CSPX from Blackrock. The US-investor alternative would be SPY, but there are many other ETF with similar characteristics. For the Bonds ETF, I would suggest studying CBU0 (Accumulating 10-year US treasuries ETF for non-US investors in USD) or IEF (Distributing 10 years US treasuries for US investors). Indeed, when most portfolio ‘advisers’ mention a 60/40 Stocks/Bonds portfolio, they are referring to Major Stock Index for Stocks, and to 10-years Government Bonds for Bonds.

In a following post, we will describe how to invest in an ETF at a minimal cost. In the meantime, what are your favourite ETFs and why? Happy investing!

Featured Image by Csaba Nagy from Pixabay

4 thoughts on “How to choose a good ETF?”